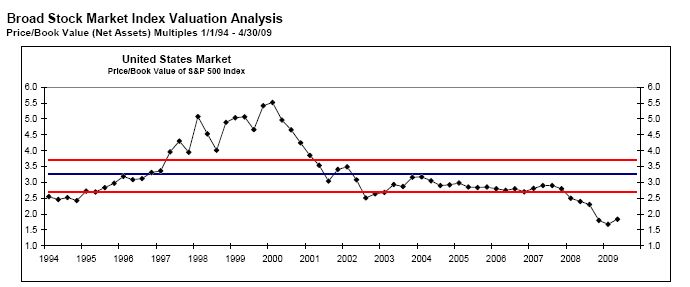

Stocks, both in the U.S. and abroad, are attractively valued from a historical perspective, but the economic challenges following the bursting of the credit bubble are daunting. This argues for a neutral (and patient) allocation to stocks in a longer-term asset allocation context.

The economy is stabilizing from the free-fall that began last September, and will likely spend an extended period at approximately the current level of economic activity, propped up by massive government intervention and stimulus, and simultaneously weighed down by private sector balance sheet rehabilitation, which will involve a multi-year process of higher savings and debt reduction.

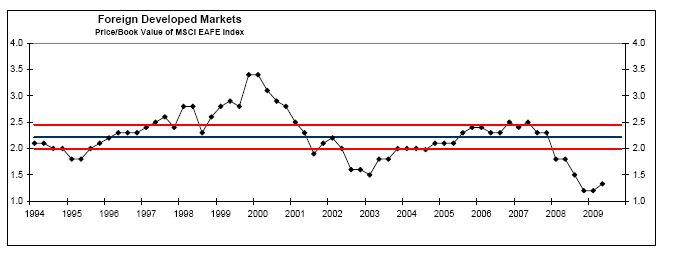

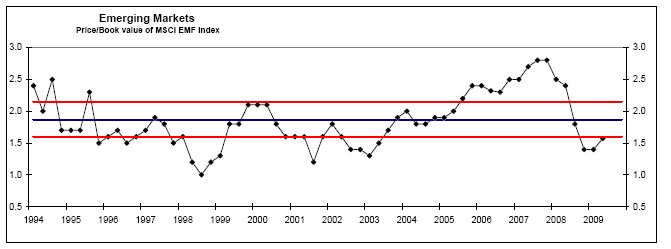

There is a strong case to be made for a healthy allocation to foreign stocks in an equity portfolio: they are cheaper than U.S stocks; key emerging markets (e.g. China and Brazil) have superior growth prospects; a number of foreign economies (both developed and emerging) have fewer problems with banking and debt; finally, there are reasons to be concerned about the U.S. dollar over a secular time frame.

发表于 2009-5-5 14:06:24

发表于 2009-5-5 14:06:24

提升卡

提升卡 置顶卡

置顶卡 变色卡

变色卡